The Best Tax Planning Strategies for Individuals in 2026

1/4/20264 min read

Effective tax planning in 2026 means doing more than filing your taxes correctly once a year. Smart taxpayers think about taxes all year long. They plan ahead and make choices that help lower taxes now and in the future.

The goal is not only to pay less this year. The real goal is to legally reduce the total taxes you pay over your lifetime while following all tax laws.

Below are practical tax planning strategies individuals should consider for 2026.

1. Adopt a Year-Round Tax Planning Approach

Many people only think about taxes when it is time to file their return. By then, most tax-saving chances are already gone. Good tax planning starts at the beginning of the year and continues every month.

Start by reviewing last year’s tax return. This helps you understand your income, deductions, and any missed opportunities. Then estimate how much income you expect to earn during the year.

Life changes can also affect your taxes. Events such as getting married, changing jobs, having a child, buying a home, or retiring can all change how much tax you owe. Planning early allows you to adjust before tax season arrives.

Taxes should also be planned together with retirement savings, investments, and long-term financial goals. When everything works together, you often save more money over time.

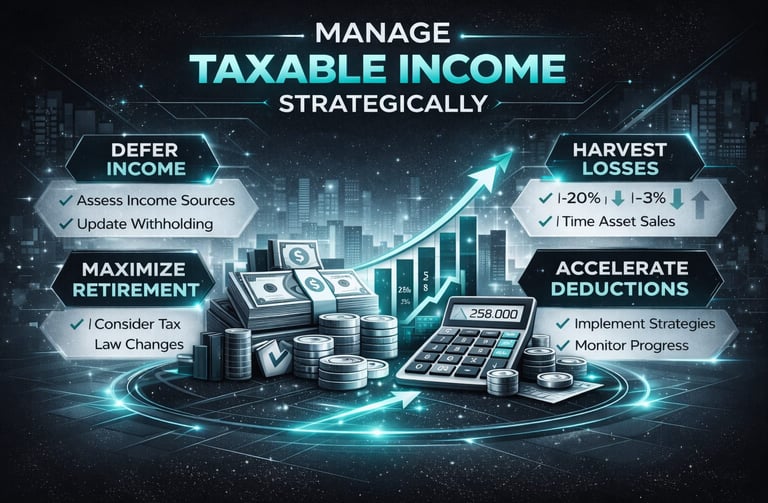

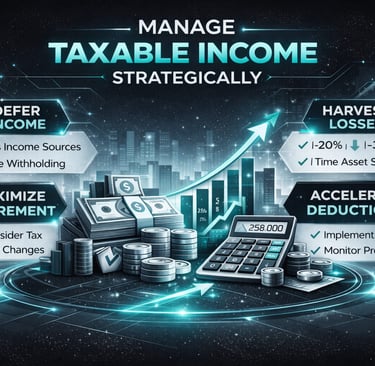

2. Manage Taxable Income Strategically

One of the best ways to lower taxes is to reduce your taxable income. Taxable income is the amount of money the government uses to calculate how much tax you owe.

Saving for retirement is a powerful way to do this. Contributions to workplace retirement plans like a 401(k) or 403(b) lower your taxable income today. At the same time, your investments grow over time until retirement. If your employer offers matching contributions, try to contribute enough to receive the full match since this is essentially free money.

Health Savings Accounts (HSAs) are another strong tax tool for people with high-deductible health insurance plans. Money you put into an HSA may lower your taxes, grows tax-free, and can be withdrawn tax-free for qualified medical expenses. Some people even use HSAs as extra retirement savings for future healthcare costs.

Traditional IRA contributions may also reduce your adjusted gross income, depending on your earnings and whether you have a workplace retirement plan. Lower income levels can help you qualify for more tax credits and deductions.

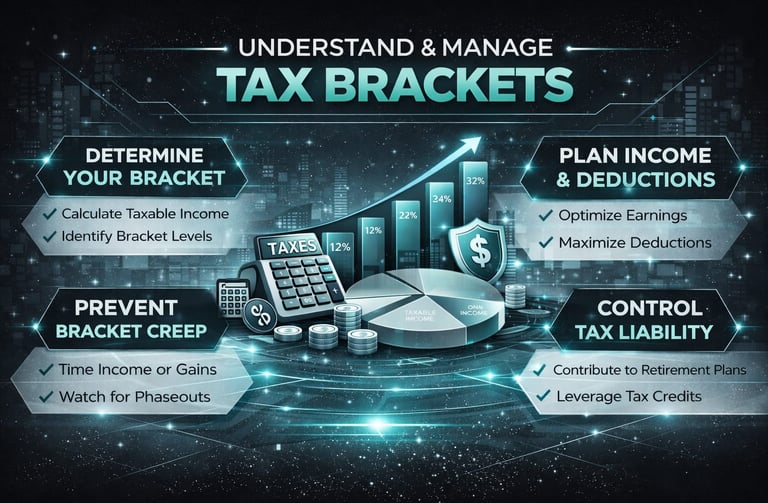

3. Understand and Manage Tax Brackets

The U.S. tax system uses tax brackets, which means different parts of your income are taxed at different rates. Knowing which bracket you fall into can help you make smarter financial decisions.

If your income is close to moving into a higher tax bracket, you may benefit from delaying income until the next year or increasing deductions in the current year. Small timing decisions can sometimes prevent higher taxes.

Roth IRA conversions are another planning option. This involves moving money from a Traditional IRA into a Roth IRA. You pay taxes on the amount converted today, but future withdrawals can be tax-free if rules are followed.

This strategy can work well during years when your income is lower than usual, such as early retirement or a job transition. However, careful planning is important so the conversion does not push you into a higher tax bracket.

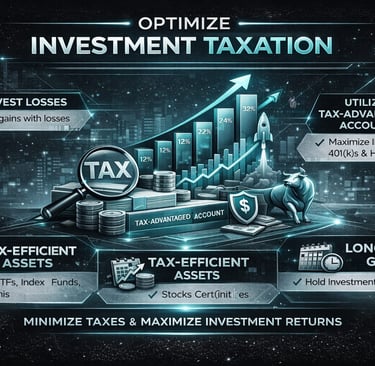

4. Optimize Investment Taxation

Investments can create taxes, so it is important to think about taxes when buying or selling assets.

Investments held longer than one year usually qualify for lower long-term capital gains tax rates. Selling too quickly may result in short-term gains, which are taxed at higher ordinary income rates. Simply holding investments longer can improve your after-tax returns.

Tax-loss harvesting is another useful strategy. If some investments lose value, selling them can create a loss that offsets gains from other investments. If losses are greater than gains, up to $3,000 can reduce regular income each year, with extra losses carried forward to future years.

Planning when to sell investments can make a meaningful difference in how much tax you ultimately pay.

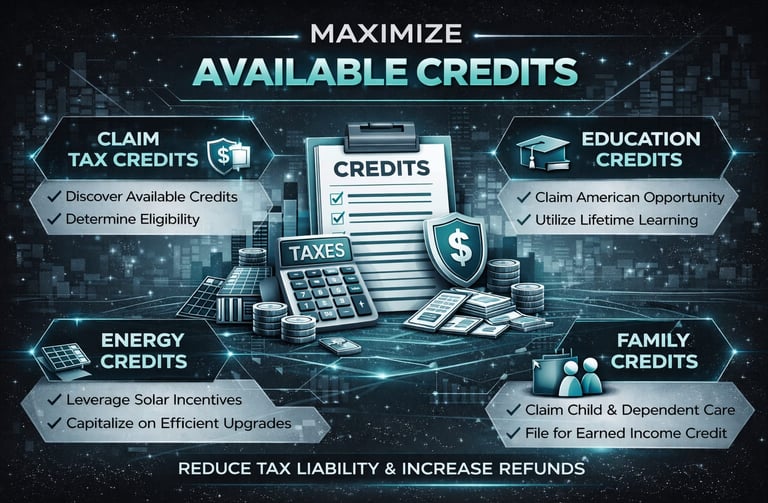

5. Maximize Available Credits

Tax credits are especially valuable because they reduce your tax bill dollar-for-dollar, not just your taxable income.

Individuals should review eligibility for credits such as the Child Tax Credit, education-related credits, and energy-efficiency incentives for home improvements or clean energy upgrades.

Many credits have income limits. This means managing your income carefully may help you remain eligible. Even small adjustments to income or deductions can sometimes allow you to qualify for valuable credits.

Checking credit eligibility each year ensures you do not miss savings that are already available under tax law.

6. Evaluate the Standard Deduction vs. Itemizing

Each year, taxpayers must decide whether to take the standard deduction or itemize deductions. Choosing the larger option usually leads to lower taxes.

Itemized deductions may include mortgage interest, state and local taxes (within allowed limits), charitable donations, and certain medical expenses. If these expenses add up to more than the standard deduction, itemizing may provide greater savings.

Some taxpayers use a strategy called “bunching,” where they group charitable donations into one year instead of spreading them out. This can help push total deductions high enough to benefit from itemizing.

Reviewing this choice annually is important because income and expenses change from year to year.

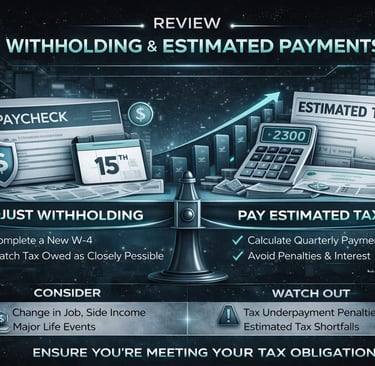

7. Review Withholding and Estimated Payments

Proper tax withholding helps avoid surprises when filing your return. If too little tax is withheld from your paycheck, you may owe money and face penalties. If too much is withheld, you are giving the government an interest-free loan.

Review your W-4 form after major income or life changes to make sure the correct amount of tax is being withheld.

People who earn income from freelance work, investments, or side businesses may need to make estimated quarterly tax payments. Staying current with these payments helps avoid penalties and keeps cash flow predictable throughout the year.

Final Thoughts

The best tax planning strategies for individuals in 2026 focus on managing income carefully, saving for retirement, making tax-smart investment decisions, and using available deductions and credits.

Tax planning is not something done once a year. It is an ongoing process that changes as your income, family situation, and financial goals evolve.

Taking a steady, year-round approach can reduce stress, lower lifetime taxes, and help build long-term financial security.

Social Connection

© 2026. All rights reserved.